Do South Asian Central Banks have currency targets?

Even if they don't want to?

(This article is part of a series exploring South Asia’s economic story as a distinct economic phenomenon. You can read the first article in this series here. Usual disclaimers apply).

Over the last few decades, central banks across the world have gradually moved towards some form or the other of inflation targeting. This has broadly gone alongside currency control generally going the other way. After the collapse of Bretton Woods and then after WTO rules came about, I think it’s fair to say that the world has had a bias towards flexible exchange rates. Exchange rate control tends to be seen with at least some level of skepticism and there are enough cases of currency manipulation accusations being thrown around. Instead, focusing on managing inflation through adjusting interest rates has increasingly become the primary policy prescription across monetary regimes aross.

Without getting into the specific histories of each country, the same gradual move towards inflation targeting regimes is true for South Asia as well. The legal strength of the inflation targeting regimes in South Asia vary, but even when it is not a strict target, these central banks have anyway tended to have a push towards managing inflation.

South Asia’s economic makeup ties its inflation closely to currency moves

This context of the economic structure of South Asia is one that has general FX deficits on trade and income. This then means that in order to bridge this, South Asia requires constant capital inflows. Where these inflows fail or change, that can then necessitate some amount of depreciation or use of FX reserves of the central bank to defend the currency. Often, this has been a combination with central bank activity mostly during changes in capital movements and currency movements during underlying changes in the economies themselves.

Does this currency depreciation then affect local inflation? In two forms, it can. One is through the fuel import side. Given South Asia is a net importer of fuel at a substantial rate, this then means that any currency pressure directly translates through to the local economy through the price of fuel. Given the direct political cost of rising fuel in the region, this also likely ties into how fiscal support for fuel imports and fuel pricing has been a constant and recurrent factor in South Asia.

The other mechanism is through the angle of food. While South Asia produces a significant amount of its food, it still has a substantial import cost as well as the cost of fertilizer, machinery and other inputs needed for the agricultural sector. To simplify, we can simply show that imports of food and fertilizer alone accounted for around 1% of GDP in 2019. Given the large amount of consumption in these economies. Again, this likely creates strong fiscal incentives towards supporting food, fertilizer, and agriculture.

Whenever the fiscal space for these protective measures exist, South Asia can manage price changes that happen from currency moves. But when the fiscal space is less strong (South Asia also has relatively weak revenue bases), the direct impact of currency movements onto the inflation dynamics is pretty straightforward.

Do South Asian Central Banks end up having implied exchange rate targets for inflation control reasons?

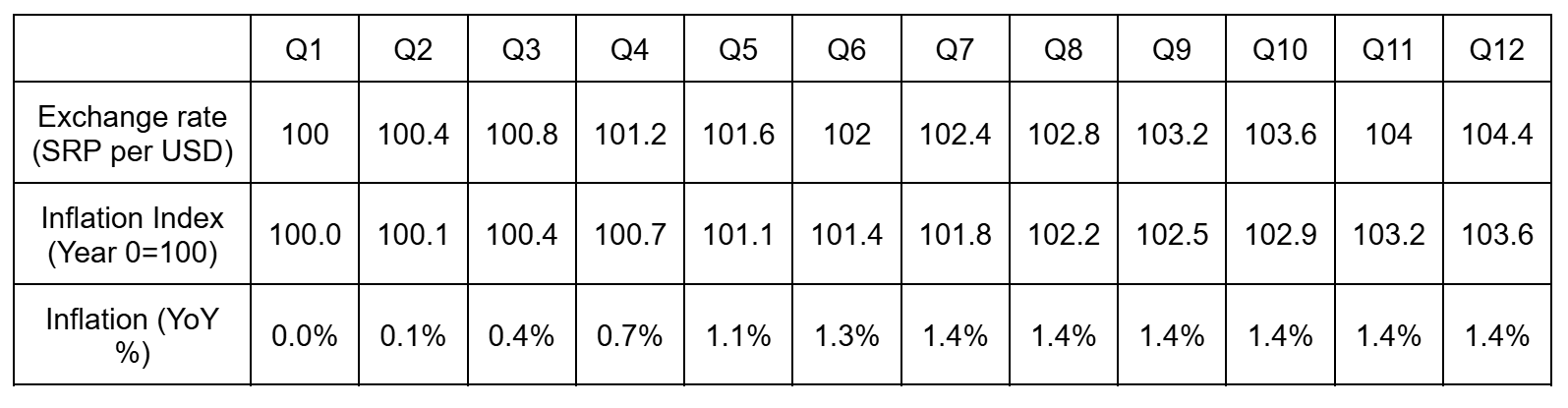

Even if this is not explicitly a target, there can be a bit of an implied target. Lets use a hypothetical currency and inflation story to showcase this. Lets assume a currency starts at 100 rupees (I’m going to be bold and call this currency the South Asian Rupee - SRP) per USD, and assume a defacto inflation target at 2%. Lets assume that for the local inflation index, about 30% is directly tied to the price of imports. Let’s assume the pass through of currency movements to inflation happens where the direct import goods (30%) is immediately inflated, and the rest of the economy that depends on these imported goods (60%) is inflated in 2 stages across 2 quarters. These may not be realistic assumptions, but I’m taking them to show the issue illustratively.

Here, if we assume the exchange rate depreciates by 1% in each quarter, we would see inflation pickup to 3% by Q6, and not really fall to the target after that. This then is a clear breach of the 2% defacto target. If the central bank wants to bring inflation back to 2% here, they would then have to act.

However, lets see what happens if the exchange rate actually depreciates at a slower rate. For whatever reason or the other, lets assume that instead of 1 SRP depreciation per quarter, there is only a 0.7 SRP depreciation instead. In such a context, the inflation rate is significantly less and doesn’t go much beyond the defacto 2% target.

Here, a simple and clear point comes about. If the central bank is meant to maintain exchange rate flexibility, then that can act against their inflation target in some cases. If the exchange rate naturally wants to go weaker, then that can easily cause inflation to go out of target. The same is true the other way, if the exchange rate sees only slight depreciation (or even appreciation), then that adds a strong disinflationary force that can take inflation the other way around as well.

Fundamentally, given the struture of South Asia’s economy, this then means that there is actually an implied “range” of exchange rate movement that can work for the economy’s inflation targets. In this illustrative example, if the exchange rate depreciates above about 0.7% per quarter, that pushes inflation too high. If the exchange rate depreciates below about 0.4% per quarter, that pushes inflation too low. For this economy then, there is an implied exchange rate depreciation range of 0.4-0.7% per quarter, or roughly 1.5% to 3% a year.

How do South Asia’s inflation regimes tie into its economic structure?

The move towards greater inflation targeting often involves greater and greater use of the monetary lever. In effect, adjusting interest rates often occurs where central banks try to maintain a particular interest rate level. In technical terms, this is a price target or price control on interest rates and credit that affects the supply of credit and thereby, affects demand. In simple terms, expensive loans=expensive business activity=slower growth=slower demand.

The issue is that in additional to an interest rate target that modern inflation targeting measures call upon, South Asia’s central banks might also have an implied exchange rate target for the same inflation targeting reason. These are not necessarily contrary goals - a particular level of interest rate and credit growth might be exactly in line with the exchange rate target for example, especially when inflation is driven by domestic demand forces.

The question comes when depreciation occurs for reasons outside domestic demand. Primarily, this would be capital flows but it could also be demand forces outside of the central bank’s jurisdiction. Given South Asia is a net importer of oil, the oil price is one clear way that this can come through.

This itself is once again, not too much of a problem in a “free market” sense. You can still adjust the interest rate to account for this, and although it might be a much tougher job given the speed of interest rate mechanisms compared to that of capital flows, its not impossible. Domestic demand will need to contract by a bigger margin that otherwise, but its still technically possible.

The issue comes with the structure of the economy, which then affects the social and political structure of the region as well. The fiscal incentives, the electoral incentives, can actually run counter to the measures needed to maintain inflation in such a context. These are not factors a central bank can, or even should in my view, get involved with.

My personal view here is that South Asia needs to have a long hard conversation of what sort of economy it wants to have, and what kind of policy measures can support that. In such a context, I think whether some amount of depreciation is okay or not is then part of a much bigger conversation. Once that economic conversation has gathered more steam, I think the question on what sort of way to support an inflation target takes a different form. If the economy decides that it wants to move towards a production-export economy for example, demand might anyway need to be weak enough that disinflation rather than inflation becomes the problem. If the economy decides it wants to run on a consumption based growth pathway, such a pathway might need to grapple on the inflationary consequences this necessitates.

In either of these context or any other, I think it becomes important to consider these varied systematic incentives that can be at play. They can push varied policy in varied directions, even if intentions remain clear and strong. Recognizing these incentives, and the fact that South Asia probably already has implied exchange rate targets to meet their inflation needs, can help understand the economy better.