80 years of the dollar

An exorbitant something-or-the-other

(There’s a lot going on in the global economy right now. Entire systems themselves might be changing. This is something I’ve been trying to write on for a good year now, but things have moved too fast for me to sit down and put something together. This article is therefore written as one part of many exploring just one aspect of the global monetary system. This first part explores an overall framing of this story - on the dollar’s status as the global reserve - before future parts will go into smaller and smaller time periods. Enough of these views are unorthodox enough that I have to place usual disclaimers on these being personal views, stronger than usual as well.)

Over the last few years, the calls of de-dollarization has started to sound a little louder than before. Regardless of whether it’s realistic or not, the idea of a world without a dollar is something that more and more and people are beginning to explore - and others to call for. Yet the dollar’s role in the global system isn’t an accident of history. Over decades, it has wrought itself to where it is today - through massive turmoil and pretty remarkable periods of stability too.

Looking at how the dollar evolved to its modern form can help frame the contemporary point a bit better. The story of the dollar in this approach is the story of the global monetary order and how it has moved and changed over time. Whether this movement will continue in the same way or whether it will change how it moves is a pretty important point in the end.

80 years of the dollar as the reserve currency of the world

Formally with the Bretton-Woods arrangements of 1944/5, but informally from at least partway through WW2. the USD was increasingly being used as the major international currency. Since then, despite all the narratives around the USSR, the Japanese, the Europeans, and now the Chinese, the dollar has reigned supreme.

What supported this? The strength of the US economy is undoubtedly a factor here - the US has been the world’s largest economy since at least the mid-1930s. For such a large economy, it has also maintained impressive enough growth rates - growing to be 50% larger than the EU despite being roughly the same size in the 1970s (although admittedly, almost all of this overperformance is since the Euro crisis).

Beyond this, there are all the softer reasons provided for the USD’s dominance. There are the military arguments, the argument that the US can maintain parity against a commodity (gold at one point, time and trust right now), and even the arguments on US soft power across the world. No doubt these have at least some impact as well. I would argue they are more consequences rather than reasons for the dollar’s dominance, but they almost definitely have at least a partial mutual impact too.

Deep USD markets almost definitely allowed the dollar to remain the global reserve

The key reason I would point to, would probably be the depth and liquidity in the US’ financial markets. The use of the USD in global transactions is itself probably the measure here that best illustrates it. Other indicators follow - since the 70s, the US has the largest amount of portfolio flows, debt flows, and even credit flows across its borders. Not just within the US, but the depth of the US markets are accessible to foreigners as well. To be a global currency, one that the rest of the world works on, this feels to me the most important. Everyone needs to have easy access to the USD for it to be a global unit of account.

This is part of what allowed the US to actually continue running this system itself. Given how much of the overall system is driven by varied financial market flows, including credit, there is a pretty huge demand and supply for USD based financing. For the US, this gives two massive opportunities. By changing local financial conditions, they have a powerful lever to move the rest of the world. But the rest of the world also has so much financial depth in the US’ own currency, that they can finance themselves regardless of what happens. The idea of the “exorbitant privilege” that being the global reserve currency, to me, is from this lens.

The “exorbitant burden” of being the global reserve currency

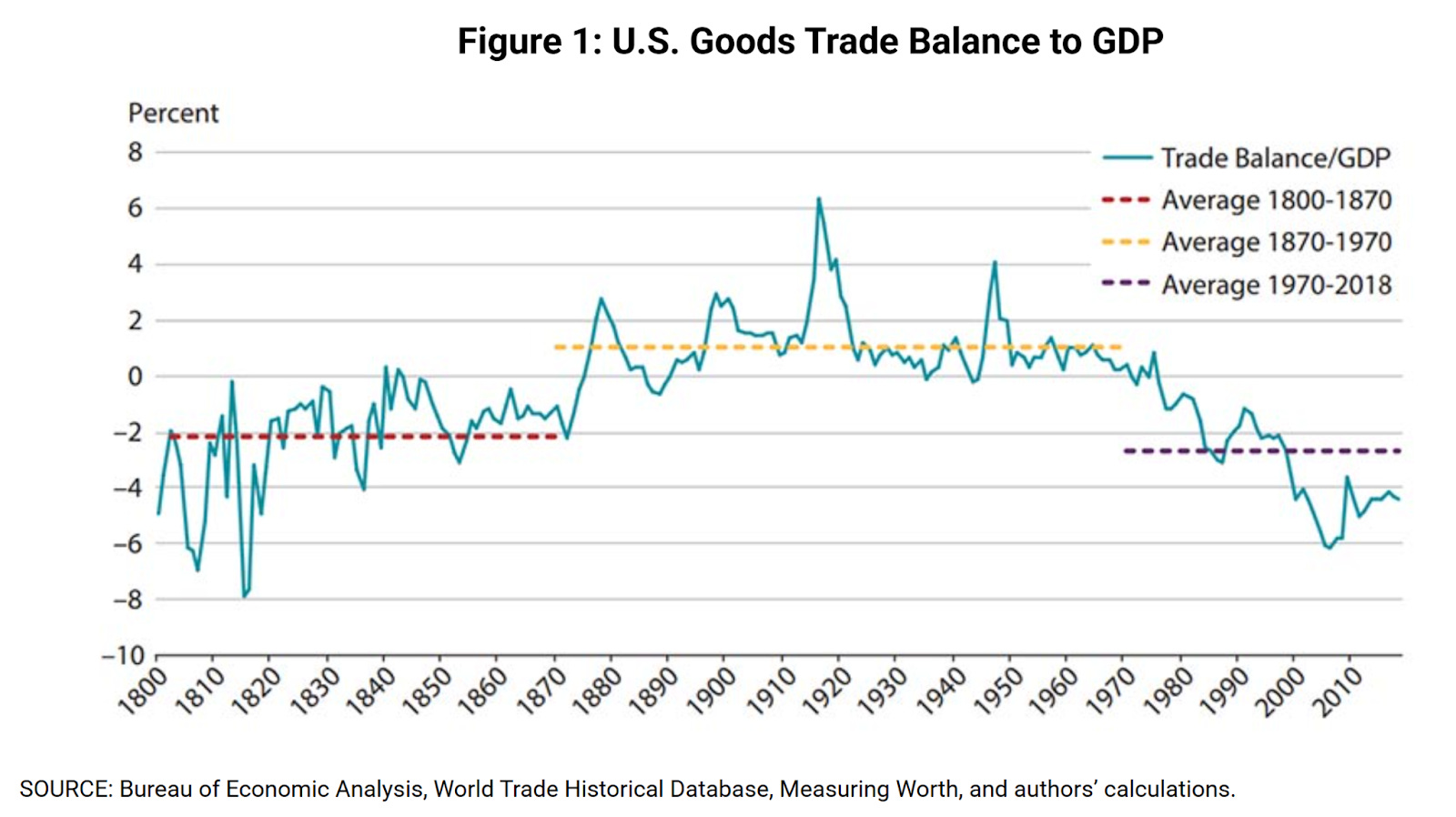

But the cost of having a currency that anyone can access? Being vulnerable to either the trade or currency (or both) impacts that people moving money across your borders will have. As people use the USD, they build up contracts of credit and otherwise, that requires them to have access to further USD to meet. This means USD flowing out of the US. Where does the US find the USD to send out? Either it has to use the results of its own production, running down its external surpluses. If they don’t have this, they need to create new USD or at least allow for new USD to be created. This means credit - which then boosts local consumption - and takes external balances into deficit. To pay down said credit, the US also now needs USD. The cycle continues until it doesn’t.

Across the 80 years since Bretton-Woods, the US has been gradually expanding its consumption in this way - first by running down its surpluses, and then by expanding deficits. The chart from the St. Louis Fed shows how this has moved on the trade account. This is the consequence of being the reserve currency - being whipped by the emotions of capital flows. Where will this go from here?

This is part of what different parties aligned with the Trump administration (I don’t think anyone can say there is anyone more than “allied” with Trump and global trade decisions!) have called the “exorbitant burden” of running the global reserve currency. This isn’t a concept that’s widely accepted - former RBI governor/IMF Chief Economist Raghuram Rajan recently wrote against this entire economic concept for example.

What keeps this system going, in my view, is not just the global capital story but how this interacts with the local econopolitical dynamics in the US and other countries. Part of this is how the credit that flows into the US isn’t simply a one to one transaction but rather mediated across many other parties in between. All this creates incentives - in the US to push domestic spending and consumption, and in counterparties to do the opposite.

At varied points in history, these incentives have led to what I consider different underlying monetary orders that have underpinned the dollar’s reserve status. We see to be in a similar place once again. Will it be a change that changes the system but keeps the dollar ascendant? Or will the mighty dollar itself start retreating this time around?

The next part of this series of essays can be found here -

The three monetary orders of the dollar system

(This article is one of a multi-part series exploring the global monetary system - starting from its past, and hopefully exploring its future. The first piece - on the dollar’s 8 decade hegemony is here. While some ideas are reflective of standard monetary history, the framing of others are ones that might be a bit new.…